Characterizes the rationality and intensity of the use of working capital in the organization.

Current assets turnover ratio calculated in the FinEkAnalysis program in the Business Activity Analysis block as the Material Assets Turnover Ratio..

Current asset turnover ratio - what it shows

Current assets turnover ratio shows the number of turnovers of material inventories.

Current assets turnover ratio - formula

General formula for calculating the coefficient:

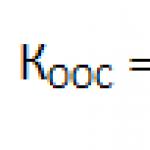

| K ooa = | Net sales revenue |

| Inventory and VAT |

| K ooa = | c.2110 Form 2 |

| (c.1210n. Form 1 + c.1210k. Form 1 + c.1220n. Form 1 + c.1220k. Form 1)/2 |

Current assets turnover ratio - value

If Current assets turnover ratio greater than 1, the enterprise can be considered profitable.

A decrease in the ratio indicates a relative increase in inventories and work in progress or a decrease in demand for finished products.

Was the page helpful?

Synonyms

More found about the current assets turnover ratio

- The relationship between the turnover of current assets and the financial condition of an economic entity

About Prigma there is a slowdown in 2014 turnover current assets So coefficient turnover decreased by 0.5 times and the duration of one revolution increased by - The influence of the turnover of assets and liabilities on the solvency of the organization

KOcon value of short-term liabilities at the end of the reporting period Coefficient turnover current assets Kobor OA in accordance with the traditional approach is determined by the ratio of the amount of revenue - Modeling the impact of an enterprise’s financial indicators on its creditworthiness

As a result of the study, the influence of the financial dependence coefficient of the coefficient was statistically confirmed turnover current assets asset coverage ratio on the creditworthiness of industrial and wholesale trade enterprises It can be assumed - Analysis of consolidated and segment reporting: methodological aspect

The following financial ratios can be proposed: share of current assets in property; share of cash and short-term financial investments in current assets; financial independence ratio; debt capital structure ratio; investment ratio; current liquidity ratio; quick liquidity ratio; absolute liquidity ratio; ratio turnover current assets ratio turnover assets return on sales profit margin return on assets return on equity ratio - Business activity indicators of Elan-95 LLC

Capital productivity of fixed assets turnover 8.7 13.7 30.7 15.3 6.5 8.1 15.1 15.7 17.8 Coefficient turnover current assets turnover 3.1 2.9 3.4 3.5 3.6 3.3 3.1 3.3 3.4 Ratio - Methodology for assessing business activity of agribusiness enterprises based on cash flow indicators

Revenue Assets Ratio turnover current assets Revenue Current assets Characterize the effectiveness of using total and current assets Growth - Assessing the effectiveness of receivables management of an organization using the example of wholesale trade organizations in the Russian Federation

Average annual amount of current assets in billion rubles 15326.25 19683.35 17507.65 19624.9 23807.3 26351.9 Coefficient turnover current assets in units 1.65 1.58 1.61 1.64 1.64 1.63 Average value of accounts payable - Assessment of business activity of an enterprise based on asset turnover indicators

B 1 2 3 1 Coefficient turnover total capital 0.889 0.842 0.605 2 Coefficient turnover current assets 1.474 1.233 1.027 3 Ratio turnover equity capital 1,819 3,069 1,839 - Analysis of financial condition in order to determine the creditworthiness of the organization

K8 coefficient of return on equity capital of net assets K9 coefficient turnover working capital characterizes the turnover rate of all working capital, both material and - Methodology for analyzing the consolidation of a cash flow statement

R 0 CA where CA is the average annual cost of current assets Cash ratio turnover accounts receivable k AR is calculated using the formula k AR R - Methodology for analyzing current assets of a commercial organization

As general indicators turnover current assets of the enterprise are allocated 1 Coefficient turnover current assets turnover current assets in times which characterizes the rate of turnover of current assets - Factors and problems of effective use of current assets in the agricultural sector

V I Chapaeva pedigree cattle breeding Coefficient turnover current assets 3.5 1.5 1.4 Duration of one turnover of current assets days 104 245 -

Therefore, when assessing and analyzing the business activity of an enterprise, it is necessary to obtain information not only in general form, coefficient turnover current assets but also analytical information which includes the values of indicators and - Ways to optimize financing of working capital at an enterprise

Decrease in coefficient turnover current assets Increase in the volume of current assets Decrease in the ratio turnover equity capital Inefficient use - Assessing the financial performance of mergers and acquisitions

Capital productivity Ф 1.36 1.25 2.45 min Coefficient turnover current assets of JSC 4.06 3.35 4.69 2.93 Coefficient turnover equity capital Eqt - The influence of the structure of working capital on the indicators of the financial condition of the organization

Aob Ko 2 where Ko is the coefficient turnover current assets Based on this, the relative change in own working capital reflects the growth rate - Improving accounting and analytical support for managing working capital of an organization

Current assets coverage ratio with own funds Ratio turnover current assets Duration of turnover of current assets Debt ratio Coefficient of consolidation of funds in turnover - Current issues and modern experience in analyzing the financial condition of organizations - part 4

The sum of the values of the proportions of the standards for the amount of reserves of receivables of cash constitutes the standard for the total amount of working capital Coefficient turnover assets is calculated using the formula COBA turnover Production output Working capital standard - The influence of individual elements of accounting policies on reporting items and financial performance indicators

Material efficiency coefficient turnover current assets 1. Procedure for writing off TZR - average interest method - simplified methods - Coefficient method in assessing cash flows

Other sales consumption % 1.463 1.331 -0.132 5 Coefficient turnover current assets 8.864 11.533 2.669 6 Current assets coverage ratio for short-term liabilities 0.597

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to know how solve exactly your problem- contact a consultant:

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and FOR FREE!

Let's figure out how to act and where to find indicators. To produce goods, it is not enough to use means of labor (machines, equipment) and employ workers.

It is necessary to have source materials, raw materials, blanks, that is, everything that is needed when creating finished products in the production process. Labor items are required.

To do this, you need to have money to purchase everything you need from suppliers and pay staff for their work.

Objects of labor and money make up the company's working capital. But you need to determine the value of such an indicator and know how to write off working capital.

Basic moments

First, let's find out what is meant by this economic expression and what regulations are relevant.

What it is

Working capital is the totality of funds that are turned over and monetary funds in circulation. Working funds are presented:

- raw materials;

- basic and auxiliary materials;

- components;

- unfinished production facilities;

- container;

- other objects of labor.

Why is it needed?

The turnover ratio of tangible working capital reflects the number of times the company used the average indicator of the available balance of working capital in the analyzed period.

According to the balance sheet, current assets consist of:

- stocks;

- money;

- short-term financial investments;

- short-term receivables taking into account purchased assets.

The values can characterize what proportion of current assets and total assets are and how effectively they are managed.

But it is worth remembering that the nuances of the industry in the production cycle are also taken into account. Working capital turnover is an important indicator.

Indeed, with the rapid turnover of company funds, the gap between the funds invested in the production process and the receipt decreases.

The difference between working capital and fixed assets is that they are used in production cycles once, and they can transfer their price to the finished product.

Regulatory regulation

It is important to study the provisions:

- PBU 6/01 according to.

- Guidelines for accounting of fixed assets (), etc.

How to determine the working capital turnover ratio

There are ready-made formulas that can be used to calculate turnover in any industry.

But in many cases it will not be possible to obtain an accurate result, since it is impossible to take into account all factors, and the management of each organization has different knowledge in the field of business.

What does it characterize

Thanks to the working capital turnover ratio, you can determine how efficiently current assets are used. You should rely on the information in the balance sheet.

The turnover ratio is a financial indicator that measures how effectively assets and liabilities are being used.

It is able to show the business activity of the organization. If the asset turnover ratio is three, it means that the company receives revenue per year that is three times the value of the assets.

Since turnover rates may depend on the industry, it is worth understanding that in a trading company with a large volume of revenue, turnover will be higher.

If the industry is capital intensive, a lower value will be obtained. But it is not correct to assume that turnover will indicate operational efficiency and profitability.

But when conducting a comparative analysis of the ratios of two organizations, you can see the difference in the effectiveness of asset management.

If the debit debt turnover rate is higher, it means that payments from customers are collected efficiently.

The main goal pursued when managing the company's assets (including working capital) is to increase the profit on invested funds, ensuring the stable and sufficient solvency of the organization.

In order for such a goal to be achieved, it is necessary to constantly have a certain amount in the account, which is actually withdrawn from circulation. Current payments are made using these funds.

Part of the amount should be placed as highly liquid assets. It is important to ensure that the optimal balance between solvency and profitability is ensured.

To do this, they maintain the size and structure of current assets, borrowed funds and their own working capital.

What are the types

The most popular ratios in financial plan analysis:

| Turnover of current assets | What is represented by the ratio of the proceeds of an enterprise in general to the turnover of the amount of assets of the organization for a specific time |

| Inventory turnover | What shows how management uses jumps in profit and cost figures |

| Accounts receivable turnover | This coefficient will allow you to calculate how much debit debt has been generated |

| Accounts payable | What is necessary for the lender, as it allows you to determine whether payment of the company’s loan is possible |

| Assets | What determines the indicators of many financial turnovers |

| Firm's equity | What can show the effectiveness of the use of funds by an organizational unit |

Formula applied

What positions characterize the coefficient? The indicator depends:

- on the duration of production cycles;

- employee qualifications;

- type of activity;

- pace (performance indicators).

A greater value is typical for trading organizations, and a lesser value for capital-intensive scientific firms.

The formulas are directly proportional equations that are easy to understand.

If you can’t figure them out, you can always contact a specialist who can help with the calculations

So, the formula for determining the asset turnover ratio looks like this:

This formula is used most often. Less commonly used is a formula in which the working capital turnover ratio is calculated as the ratio of the number of days in a year to the capital turnover data.

Any value can be quickly found. For example, information about assets is in the balance sheet, and information about revenue is in the cash statements of the enterprise.

And here is the formula for the current assets turnover ratio:

If the value is large, then we can talk about the growth of the enterprise. Current assets are not taken into account at the beginning/end of the period, which is analyzed. The average annual balance is important.

The numbers for the beginning of the year and the end must be divided by two. In addition to the material turnover ratio, the turnover rate is also determined in days that one turnover can take.

So 365 days should be divided by the annual turnover ratio. For example, a coefficient figure of 3 will show that assets turn over in 121.7 days.

What are the features of calculating the capital turnover ratio of a company? There are no specific rules, just like there is no average value.

Each organization produces its own values, which will be different (depending on the industry). But there is a direct relationship - the higher the coefficient, the higher the return on capital will be.

The formula is:

The company must be able to use intensively inventories and costs to its advantage. Use the formula:

If a high value is obtained, it means that the company does not have enough inventory. As a result, unnecessary waste appears.

Formula for determining the debit debt ratio:

There is no average. Everything will depend on the management and industry of the company. The higher the number, the faster the company can pay off its debts.

When determining the loan debt turnover ratio, use the formula:

The result will show how intensively the company repays its debts. There cannot be a specific overall value for the coefficients.

They are analyzed over time or compared with the indicators of another enterprise in this industry.

If the value is very low and cannot be justified by the characteristics of the industry, it means that the company has excess working capital. If the indicator increases, most often this is a plus for the company.

The turnover of mobile funds will be fast and there will be more proceeds. As turnover accelerates, other performance indicators improve.

Disadvantage - if there is a lot of inventory, it is necessary to organize storage space, which will entail additional costs.

By accelerating turnover, productivity will increase, which means more employees.

Video: determining the efficiency of using working capital of an enterprise

This means that even before planning to increase the ratio, it is worth adjusting the potential profits and costs, which will also increase.

When might turnover decrease? – If the duration of turnover increases due to an unjustified increase in inventories, the emergence of customer debts, and production failures.

After all, as a result, the production of the goods will not be completed. There may also be another reason - demand decreases, and finished goods remain in warehouses longer. Production volume is decreasing.

How to calculate by balance

To set the turnover ratio, you should take information from.

The available information will allow you to find out the value for the year. Any other period cannot be determined from the balance sheet information.

The following formula is relevant:

Let's look at it with an example. The final indicator (with line code 1200) at the end of 2015 is 400 thousand, and in 2016 – 500 thousand. The amount of revenue (with code 2110) at the end of 2015 is 1.5 million, and in 2016 – 1.8 million.

The calculation is as follows:

So, the value of the coefficient is 4, which means that the mobile fund is taken 4 times per year.

Examples of calculations

For example, in a year the company sold 5,000 units of products. The cost of one unit is 180,000 rubles. Selling price exceeds cost by 15 percent.

The average annual working capital balance is 145,000,000 rubles. You should set the coefficient value, and also find out how long one revolution lasts and what the load factor is.

This means that for one ruble of goods sold there are 14 kopecks. value of working capital inventories. One revolution lasts:

Here's another example. The Stepashka organization in 2014 had a profit of 249,239 rubles. The asset turnover indicator at the beginning of the year was 48 thousand rubles, at the end - 34 thousand.

When determining this coefficient, an indicator is obtained that characterizes the number of inventory turns over a certain time interval. This coefficient indicates how many times over a certain period of time this or that type of inventory makes a complete circuit, i.e., it reflects inventory turnover.

Calculation of inventory turnover ratio

There are two options for calculating this indicator:

- at cost of sales;

- by sales revenue.

In the first option, when determining inventory turnover, the numerator reflects the cost of sales, and the average value of inventory for the analyzed period is substituted into the denominator of the formula.

To ob. inventory = Cost of sales / Average enterprise inventory cost

With another option for calculating this coefficient, the numerator does not reflect the cost of sales, but revenue and the coefficient is calculated as follows:

To ob. inventories = Revenue / Average cost of enterprise inventories

In turn, the average value of an enterprise’s inventories is determined by the arithmetic average, i.e., by the formula:

Average inventory value = (inventory value at the beginning of the period + inventory value at the end of the period) / 2.

Calculation of inventory turnover ratio based on financial statements

From the financial results report, the numerator of the formula is filled with the indicator of line 2120 “Cost of sales”. From the balance sheet to calculate the average value of inventories, information is reflected on line 1210 “Inventories”.

The calculation of the average value of inventories according to the balance sheet is as follows:

Average value of inventories = (line 1210 “Inventories” at the beginning of the period + line 1210 “Inventories” at the end of the period) / 2.

According to financial statements, the formula for calculating the inventory turnover ratio is as follows:

To ob. inventory = line 2120 “Cost of sales” / Average line 1210 “Inventory”

If the “revenue” indicator is taken as the numerator for calculating this coefficient, then the formula looks like this:

To ob. inventory = line 2110 “Revenue” / Average line 1210 “Inventories”

The duration of one inventory turnover in days means

In addition to the number of turnovers of inventories, their turnover is measured by the circulation time or turnover duration and is expressed in days of turnover. To determine the duration of one inventory turnover in days, the turnover ratio (in revolutions) and the number of days in the period are used. The number of days in a period is taken to be 360 or 365.

The number of days (duration) during which inventories complete one turnover is calculated using the formula:

Duration of 1 inventory turnover = (Accepted annual number of days * Average enterprise inventory value) / Cost of sales

Duration of 1 inventory turnover = (Accepted annual number of days * Average value of enterprise inventories) / Revenue

If the inventory turnover ratio is already known, then the duration of 1 inventory turnover is found as follows:

Duration of 1 inventory turnover = Accepted annual number of days / K volume. reserves

A decrease or increase in turnover ratios shows

An increase in turnover time indicates a decrease in inventory turnover.

An increase in the rate of inventory turnover (i.e., the turnover ratio) means an increase in demand for goods, finished products of the enterprise, a decrease - overstocking or a decrease in demand.

Example of calculating inventory turnover ratio

The initial data for calculating the coefficient and duration of turnover are presented in Table 1.

Table 1

The average value of inventory is determined and the data is entered into the table:

2014 = (50406 + 50406) / 2 = 50406 thousand rubles.

2015 = (50406 + 57486) / 2 = 53946 thousand rubles.

2016 = (57486 + 72595) / 2 = 65040.5 thousand rubles.

Based on the table data, this coefficient is calculated:

To ob. reserves 2014: 306428 / 50406 = 6.07 revolutions;

To ob. reserves 2015: 345323 / 57486 = 6.40 revolutions;

To ob. reserves 2016: 293016 / 65040.5 = 4.50 revolutions.

Based on the calculated inventory turnover ratio, the duration of inventory turnover is calculated:

2014: 360 / 6.07 = 59.30 days;

2015: 360 / 6.40 = 56.25 days;

2016: 360 / 4.50 = 80 days.

In 2015, compared to 2014, we can talk about an increase in the business activity of the enterprise, since the duration of one inventory turnover decreased by 3.05 days (from 59.30 days to 56.25 days), and the inventory turnover increased by 0.33 times (from 6.07 revolutions to 6.40 revolutions). The data in Table 2 indicate a slowdown in inventory turnover and a decrease in business activity of the enterprise in 2016 compared to 2015: inventory turnover decreased by 1.9 turns (from 6.40 turns to 4.50 turns), and the duration of inventory turnover increased by 23.75 days (from 56.25 days to 80 days), which is a negative trend and indicates a decrease in demand for finished products or goods that are included in the company’s inventories.

Turnover ratios and inventory turnover times calculated from cost of sales and revenue will differ significantly from each other due to the excess of revenue over cost of sales.

The effective functioning of any enterprise is impossible without the competent and rational use of working capital. Depending on the type of activity, stage of the life cycle, or even the time of year, the amount of working capital an organization has may vary. However, it is the availability and proper use of these resources that determines how successful and long-lasting the activities of any business entity will be.

In order to assess the correct use of a company's working capital, there are many coefficients that analyze the speed of circulation, sufficiency, liquidity and many other equally significant characteristics. One of the most important indicators necessary to determine the financial condition of an organization is the working capital turnover ratio.

Turnover ratio (K rev), or turnover rate, shows how many times during the period of time under study the enterprise is able to completely turn over its own working capital. Thus, this value characterizes the efficiency of the company. The larger the value obtained, the more successfully the company uses its available resources.

Formula and calculation

The turnover ratio shows the number of revolutions made by working capital over the period of time under consideration. It is calculated as:

Where:

- Q p is the volume of products sold at the organization’s wholesale prices excluding VAT;

- F ob.av. – the average balance of working capital found during the period under study.

If we recall the approximate form of the cash circulation cycle at an enterprise, it turns out that the money that an organization invests in the work of its company returns to it after some time in the form of finished products. The company sells these products to its customers and again receives a certain amount of money. Their value is the income of the organization.

Thus, the general scheme “money-product-money” implies the cyclical nature of the company’s activities. The turnover ratio in this case shows how many similar turnovers the organization’s funds can make in a certain period of time (most often in 1 year). Naturally, for the effective and fruitful operation of an enterprise it is necessary that this value was as large as possible.

Necessary indicators for calculation

The working capital turnover ratio can be determined using the data presented in the financial statements of the organization. The quantities needed to determine it are shown in the first and second forms of financial statements.

So, in the general case, the volume of products sold is calculated as the revenue received by the organization in one cycle (since in most cases an annual coefficient is used for analysis, in the future we will take into account the time period t=1). Revenue for the specified period is taken from the income statement (formerly the income statement), where it is shown in a separate line as the amount received by the enterprise from the sale of work, goods or services.

The average balance of working capital is found from the second section of the balance sheet and is calculated as:

Where F 1 and F 0 are the amounts of the company’s working capital for the current and past periods of time. Note that if the calculations use data for 2013 and 2014, then the resulting coefficient will represent the rate of funds turnover specifically for 2013.

In addition to the turnover ratio in economic analysis, there are other values that analyze the turnover rate of an organization’s working capital. Many of them are also closely related to this indicator.

Thus, one of the values accompanying the turnover ratio is duration of one revolution (T rev). Its value is calculated as the quotient of dividing the number of days corresponding to the analyzed period (1 month = 30 days, 1 quarter = 90 days, 1 year = 360 days) by the value of the turnover ratio itself:

Based on this formula, the duration of one revolution can also be calculated as:

Another important indicator used when analyzing the financial condition of an organization is utilization rate of funds in circulation K load. This indicator determines the amount of working capital required to receive 1 ruble of revenue from product sales. In other words, the coefficient shows how many percent of the organization’s working capital falls on one unit of the final result. Thus, in another way the load factor can be called the capital intensity of working capital.

It is calculated using the following formula:

As can be seen from the methodology for calculating this indicator, its value is the inverse of the value of the turnover ratio. And this means that the lower the load indicator, the higher the efficiency of the organization.

Another generalizing factor in the efficiency of using working capital is the value profitability (R ob.av.). This ratio is characterized by the amount of profit received for each ruble of working capital and shows the financial efficiency of the organization. The formula for calculating it is similar to the values used to find the turnover ratio. However, in this case, instead of revenue from sales of products, the enterprise’s profit before tax is used in the numerator:

Where π is profit before tax.

Also, as in the case of the turnover ratio, the higher the return on capital value, the more financially stable the enterprise’s activities.

Turnover ratio analysis

Before moving on to analyzing the turnover ratio itself and looking for ways to increase the efficiency of an organization, let’s define what is generally meant by the concept of “working capital of a company.”

Working capital of an enterprise is understood as the amount of assets that have a useful life of less than one year. Such assets may include:

- stocks;

- unfinished production;

- finished products;

- cash;

- short-term financial investments;

- accounts receivable.

In most cases, the turnover ratio in a company has approximately the same value over a long period of time. This value may depend on the types of core activities of the company (for example, for trade enterprises this indicator will be the highest, while in the field of heavy industry its value will be quite low), its cyclical nature (some companies are characterized by a surge in activity in certain seasons) and many other factors.

However, in general, in order to change the value of this ratio and increase the efficiency of using the company’s assets, it is necessary to competently approach the working capital management policy.

Thus, a reduction in inventories can be achieved through a more economical and rational use of resources, reducing the material intensity of production and the amount of losses. In addition, significant improvements can be achieved through more efficient supply management.

The amount of work in progress is reduced by rationalizing the production cycle and reducing the cost of inventory. And reducing the amount of finished products in stock can be achieved with the help of more advanced logistics and aggressive marketing policies of the organization.

The amount of work in progress is reduced by rationalizing the production cycle and reducing the cost of inventory. And reducing the amount of finished products in stock can be achieved with the help of more advanced logistics and aggressive marketing policies of the organization.

Note that a positive impact on even one of the values presented above already has a significant impact on the turnover ratio. In addition, it is possible to achieve an increase in the efficiency of using working capital at an enterprise in indirect ways. Thus, the value of the indicator will be higher with an increase in the organization’s profit and sales volumes.

If, when plotting the dynamics of the turnover ratio over a long period of time, one can note a stable decrease in its value, this fact may be a sign of a deterioration in the financial condition of the company.

Why might it be declining?

There are several reasons for reducing the turnover ratio. Moreover, its value can be influenced by both external and internal factors. For example, if the general economic situation in the country worsens, the demand for luxury goods may fall, the appearance of new models of electrical equipment on the market will reduce the demand for old ones, and so on.

There may also be several internal reasons for a decrease in turnover rate. Among them it is worth highlighting:

- errors in working capital management;

- logistics and marketing errors;

- growth of the company's debt;

- use of outdated production technologies;

- change in the scale of activity.

Thus, most of the reasons for the deterioration of the situation at the enterprise associated with management errors and low qualifications of workers.

At the same time, in some cases, the value of the turnover ratio may decrease due to the transition to a new level of production, modernization and the use of new technologies. In this case, the value of the indicator will not be associated with the low efficiency of the company.

Let's consider a certain organization "Alpha". Having analyzed the company’s activities for 2013, we learned that revenue from sales of products at this enterprise amounted to 100 thousand rubles.

At the same time, the amount of working capital was equal to 35 thousand rubles in 2013 and 45 thousand rubles in 2012. Using the data obtained, we calculate the asset turnover ratio:

Since the resulting coefficient is 2.5, we can note that in 2013 the Alpha company had the duration of one turnover cycle:

Thus, one production cycle of the Alpha enterprise takes 144 days.

The working capital turnover ratio shows how many times the company used the average balance of working capital during a selected period of time. In this article we will use examples to understand how to correctly calculate and evaluate the indicator. We have also provided a procedure for analyzing turnover, which can be downloaded.

What is the working capital turnover ratio

The turnover ratio of working capital (assets) is an indicator that allows you to understand how many times the company used the average annual balance of working capital for a selected time interval.

CFOs analyze this indicator over time, in comparison with industry averages.

Calculation formula

The indicator is calculated using the following formula:

Working capital turnover ratio = Revenue (rub.) / Current assets (rub.). .

How to find a balance sheet

Calculation formula based on balance sheet data:

Ratio Analysis

The turnover ratio is analyzed:

- in dynamics,

- in comparison with industry averages, for example with the industry average turnover period.

A too low ratio, not justified by industry characteristics, indicates excessive accumulation of working capital. There are no generally accepted, let alone legally established standards, but this does not prevent them from being put into effect by internal administrative documents as target values or key performance indicators.

Working capital turnover period

To analyze working capital, it is often more convenient to calculate the turnover period - the reciprocal of the turnover ratio:

Working capital turnover period (days) = Number of days / Turnover ratio

This is a more visual indicator, it is measured in days and shows us how many days the company receives revenue equal to the average amount of working capital. When turnover slows down, the turnover period increases, and when it accelerates, it shortens. If we calculate the turnover period for two different time intervals and compare them, we will be able to determine the amount of additionally necessary, or vice versa, released funds.

Special mention should be made about the time interval for calculation. Turnover ratios are calculated over a certain period of time. It doesn’t have to be a whole year, as they say in textbooks. To solve practical problems, you can calculate both for half a year and for a quarter, the main thing is that this interval is sufficiently indicative and includes all factors significant for the production process. Which interval to choose depends on the industry, type of product, duration of the production cycle and terms of mutual settlements, and so on.

Calculation example

Now let's explain all of the above with an example. Suppose our enterprise produces products for which demand has significant seasonal fluctuations. During the year, the company received revenue (see table 1).

Table 1. Annual revenue of the enterprise

The average inventory during this year is presented in Table 2.

table 2. Average inventory

Let's calculate the inventory turnover ratio for the year. To do this, divide the revenue for the year by the average annual inventory.

Turnover ratio for the year = 114,830 / 36,411 = 3.154

We find that the indicator for the year is 3.154.

Let's determine the turnover period.

Turnover period = 365 days / 3.154 = 115.7 days.

It is in 115.7 days that we receive revenue equal to the average annual inventory. What will this give us in practice? We can only compare these figures with those of the previous year or go to competitors. If they tell us that their inventories turn over at approximately the same speed, we can rest assured that our indicator corresponds to the industry average.

If we calculate the data for each quarter, we will obtain additional information (see Table 3).

Table 3. Calculation of turnover ratios for each quarter

We see that inventory turnover varies greatly throughout the year. This will become even more clear if we translate the dimensionless coefficient into the turnover period (Table 4).

Table 4. Turnaround period

It turns out that the turnover rate during the year can change by one and a half times. And this can already say a lot. For example, if a company sells goods with deferred payment, then its most acute need for working capital will be at the end of the second and third quarter. If there is no deferment for buyers, then a shortage of working capital is possible from the end of the first and throughout the second quarter.

Thus, to determine the need to attract additional working capital by the beginning of the “high” season, turnover ratios should be calculated not for the year, but for the quarter.

Then we will have a completely natural desire to speed up inventory turnover in the first half of the year. To do this, it is necessary to detail the calculations by type of goods. We download the corresponding balance sheets from the program or request from the accounting department and after some processing we receive revenue for the goods (Table 5).

Table 5. Revenue by goods ()

|

Revenue, million rubles |

I quarter |

II quarter |

III quarter |

IV quarter |

Total for the year |

|

Product "A" |

|||||

|

Product "B" |

|||||

|

Product "B" |

|||||

We average inventory and obtain the following data (Table 6).

Table 6. Average stock

|

Average inventory, million rubles. |

I quarter |

II quarter |

III quarter |

IV quarter |

Total for the year |

|

Product "A" |

|||||

|

Product "B" |

|||||

|

Product "B" |

|||||

We divide the revenue for goods by the average stock, we get the turnover ratio (Table 7).

Table 7. Turnover ratio

|

Turnover ratio |

I quarter |

II quarter |

III quarter |

IV quarter |

Total for the year |

|

Product "A" |

|||||

|

Product "B" |

|||||

|

Product "B" |

|||||

|

By product group |

And now we discover that product “B” is an outsider, its turnover is two or more times lower than that of product “B” and product “A”. For greater convenience, let us convert the dimensionless coefficients into turnover periods (Table 8).

Table 8. Turnaround period

|

Turnaround period |

I quarter |

II quarter |

III quarter |

IV quarter |

Total for the year |

|

Product "A" |

|||||

|

Product "B" |

|||||

|

Product "B" |

|||||

|

By product group |

Now we see that turnover changes not only for different products, but also each product turns over at a different rate during the year.

Next, you need to find out what the reasons for such fluctuations in turnover are. If these reasons are objective and fully justified from a business point of view, then you should plan to raise additional funds when necessary. If the reasons are subjective, then organizational measures must be taken to eliminate them. At this stage, the financial analyst needs to demonstrate the ability to effectively interact with management and other departments, and the financial director needs to demonstrate his management talents.

conclusions

Turnover ratios in skillful hands become an effective tool for solving problems of financial stability of an enterprise (